Press Release

|January 23,2026Growth In Private Home And HDB Resale Flat Prices Touched Multi-Year Low In 2025, While Housing Demand Stayed Resilient, Settling Into A Goldilocks Market

Share this article:

FOR IMMEDIATE RELEASE

23 January 2026, Singapore - Latest real estate statistics showed that private home prices climbed at its slowest pace in five years in 2025, amid a rebound in transactions. Meanwhile, the HDB resale price growth has moderated to a six-year low in 2025, as the resale flat sales volume weakened. The trends collectively suggest that the Singapore housing market have perhaps settled into a Goldilocks phase, where it is not too hot, not too cold but just right - in that prices have stabilised while demand and buyer confidence remained resilient.

Q4 2025 URA Private Residential Property Index

Prices of private homes rose by 0.6% QOQ in Q4 2025, easing from the 0.9% QOQ growth in the previous quarter (see Table 1). The increase is a shade lower than the flash estimates of a 0.7% QOQ uptick published on 2 January 2025. This is the fifth consecutive quarter of price increase and overall private home prices saw a cumulative growth of 3.3% in 2025 - slowing from the 3.9% increase posted in 2024. The 3.3% price increase in 2025 is the slowest growth since 2020, where private home prices rose by 2.2%.

Table 1: URA Private Property Price Index (PPI)

Price Indices | Q1 2024 | Q2 2024 | Q3 2024 | Q4 2024 | Q4 2024 | Q1 2025 | Q2 2025 | Q3 2025 | Q4 2025 | Q4 2025 |

(QOQ % Change) | (YOY % Change) | (QOQ % Change) | (YOY % Change) | |||||||

Overall PPI | 1.4 | 0.9 | -0.7 | 2.3 | 3.9 | 0.8 | 1.0 | 0.9 | 0.6 | 3.3 |

Landed | 2.6 | 1.9 | -3.4 | -0.1 | 0.9 | 0.4 | 2.2 | 1.4 | 3.4 | 7.6 |

Non-Landed | 1.0 | 0.6 | 0.1 | 3.0 | 4.7 | 1.0 | 0.7 | 0.8 | -0.2 | 2.3 |

CCR | 3.4 | -0.3 | -1.1 | 2.6 | 4.5 | 0.8 | 3.0 | 1.7 | -3.5 | 1.9 |

RCR | 0.3 | 1.6 | 0.8 | 3.0 | 5.8 | 1.7 | -1.1 | 0.3 | 0.7 | 1.6 |

OCR | 0.2 | 0.2 | 0.0 | 3.3 | 3.7 | 0.3 | 1.1 | 0.8 | 1.0 | 3.2 |

_

Private home prices

During the quarter, the landed homes segment posted the steepest price increase at 3.4% QOQ, extending the growth streak to four quarters - culminating to an eighth successive year of price increase at 7.6% in 2025. Meanwhile, non-landed private home prices dipped by 0.2% QOQ in Q4 2025, resulting in a full-year price growth of 2.3% which is the slowest yearly increase since the 1.9% growth recorded in 2019.

Within the non-landed private homes segment, prices in the Rest of Central Region (RCR), and Outside Central Region (OCR) rose by 0.7% QOQ and 1.0% QOQ in Q4 2025, respectively - reflecting an annual price increase of 1.6% in the RCR and 3.2% in the OCR. Both RCR and OCR private home prices have now risen for nine consecutive years since 2017, albeit at a slower pace of late. This indicates underlying strength in the two sub-markets, with demand more heavily supported by Singaporean buyers. Over in the Core Central Region (CCR), private home prices fell by 3.5% QOQ in Q4 2025, but still rose by 1.9% in the full-year 2025 - marking its fifth straight year of price growth.

Private residential property transactions

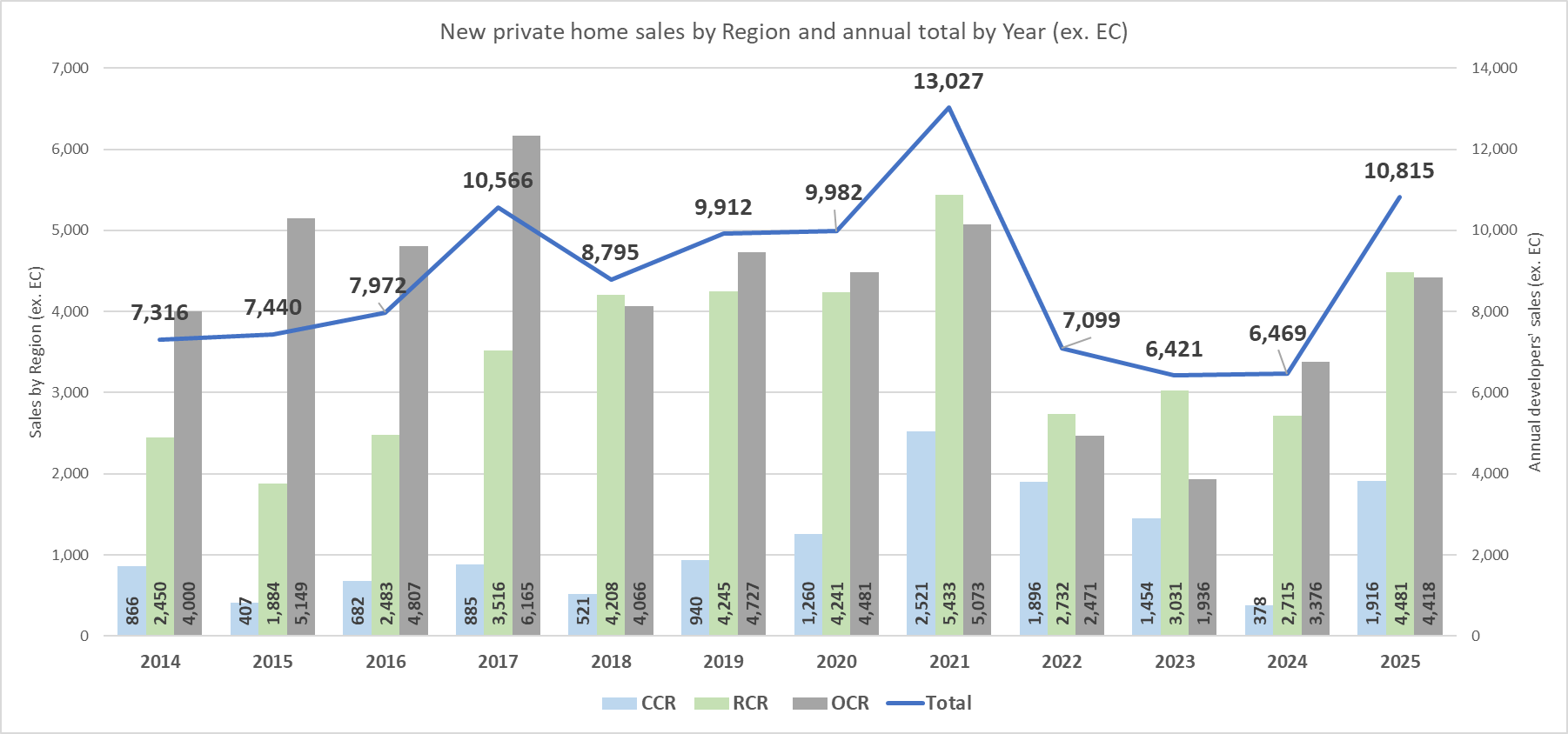

In Q4 2025, developers sold 2,940 new private homes (ex. EC), down by 10.6% from 3,288 units shifted in the previous quarter. There were a total of 10,815 new homes (ex. EC) sold in 2025, comprising 1,916 units in the CCR, 4,481 units in the RCR, and 4,418 units in the OCR (see Chart 1). The sales tally in 2025 was 67% more than the 6,469 units sold in 2024. Developers' sales hit a four-year high in 2025 amid the substantial moderation in interest rates, ample supply of new launches, competitive pricing, and improved market sentiment. During the year, developers launched 11,482 private homes and 1,360 new EC units for sale - higher than the 6,647 private homes and 1,016 EC units launched in 2024.

Chart 1: New private residential units sold by developers by Region and annual total (ex. EC)

Over in the EC segment, there were 80 new EC units sold in Q4 2025, taking the 2025 tally to 1,630 units, about 33% higher than the 1,227 new ECs sold in 2024. PropNex expects sales of ECs to remain elevated in 2026, with up to five new EC projects potentially in the launch pipeline. First to kick things off, Coastal Cabana EC in Pasir Ris sold 66.5% (498 units) of its 748 units over its launch weekend (17-18 January).

For the private residential resale market, URA data indicated that 3,529 homes were resold in Q4 2025, easing by about 9% from 3,881 units transacted in the previous quarter. In 2025, a total of 14,622 resale private homes were sold, up by 4% from 14,053 units resold in 2024. This is the highest private resale volume in four years since 19,962 were sold in 2021.

Private home rentals

Private home rentals, posted a 0.5% QOQ decline in Q4 2025, reversing the 1.2% QOQ growth in the previous quarter. This took the overall rental growth to 1.9% in the whole of 2025, recovering from the 1.9% fall in rentals in 2024, according to the URA private residential rental index. The rental recovery in 2025 reflects the tight rental stock and healthy home leasing demand. Based on URA Realis data, the number of private home rental contracts (landed and non-landed) rose to a three-year high in 2025 at 89,376 contracts - up from 82,268 and 86,476 contracts in 2023 and 2024, respectively.

PropNex expects private home rentals may continue to see marginal single-digit growth in 2026, amid stable new completions. In 2026, it is projected that 6,083 new private residential units (ex. EC) may be completed, relatively on par with 6,123 units completed in 2025. URA figures showed that the supply of new completions (ex. EC) will continue to rise in the coming years, to 8,757 units in 2027 and 10,101 units in 2028.

Mr Kelvin Fong, CEO of PropNex said:

"Looking at 2025, we believe it has been a relatively good place for the market, where prices rose more slowly despite stronger private home sales, while rentals recovered slightly amid healthy leasing demand. A combination of these indicators suggests that the market could be in a "Goldilocks" phase where it is not too cold, nor too hot but balanced and just right. That the robust sales in 2025 did not lead to rapid price spikes also reflects developers' discipline in pricing units, and their focus on driving healthy take-up rates at launch with well-calibrated prices in a highly value-conscious market.

We expect the stability and the sales momentum last year could spill into 2026. The continued moderate interest rates will help to anchor confidence and improve affordability, encouraging genuine buyers to enter the market. As at 23 January 2026, the 3-Month Compounded SORA (Singapore Overnight Rate Average) which banks use to price home loan packages stood at around 1.14% p.a., the lowest since July 2022. To this end, we note that some 2-year fixed-rate home loan packages are going at 1.4% to 1.5% p.a. currently, markedly lower than more than 4% p.a. at the end of 2022 which can help to lighten debt burdens.

Of note, we observe that the proportion of sub-sales to total sales has remained relatively low at 3.4% in Q4 2025 - among the lowest proportions in recent years. For the whole of 2025, there were 1,055 sub-sales transactions, lower than 1,428 transactions in 2024 and 1,294 sub-sales deals in 2023. Falling sub-sales - commonly seen as a proxy for property speculation - may indicate that buying activity is increasingly driven by owner-occupiers and purchasers who take a longer-term view, which will be positive for market stability. Fewer sub-sales could also mean that buyers have stronger financial holding power, or face less financing stress due to high interest rates.

Another factor that we expect could be supportive of the market in 2026 is the relatively low unsold stock in the market. According to URA data, there were 14,859 unsold, uncompleted private homes (ex. EC) in the pipeline at the end of Q4 2025, down by 12.7% from 17,029 units (ex. EC) in Q3 2025 and it is the lowest figure in 15 quarters. Given an annual 10-year average developers' sales (2016 to 2025) at 9,106 units (ex. EC) per year, the unsold inventory may potentially be absorbed by the market in around two years.

According to latest estimates (23 Jan) from the PropNex sales team, about 8,800 units of private homes (ex. EC) from 23 projects and five EC projects with some 2,300 new EC units may be launched in 2026. Of those, Coastal Cabana EC has already been put on the market, while Narra Residences and Newport Residences will be launched later this month.

With moderating price growth and low interest rates, we believe that there is a window of opportunity in 2026 for prospective buyers, including HDB upgraders to purchase private homes. To this end, some HDB flat owners may consider selling their flat - as HDB resale price growth flattens - and upgrade to a private residential property amid stabilising private home prices.

In 2026, PropNex projects that developers' sales may range from 8,000 to 9,000 units (ex. EC) - likely coming in at the upper-end of the forecast - while private resale transaction volume may come in at about 14,000 to 15,000 units. Meanwhile, we expect private home prices could continue to grow moderately at 3% to 4% in 2026."

Q4 2025 HDB Resale Price Index

Data from the Housing and Development Board (HDB) showed that resale flat prices were flat in Q4 2025, following a trim 0.4% growth in Q3 2025 (see Table 2). This is the first time that HDB resale prices were unchanged since Q1 2020. Overall, HDB resale prices rose by a cumulative 2.9% in 2025 - the slowest pace of increase since 2019 where prices inched up by 0.1%. The final print is on par with the flash estimates released earlier in the month.

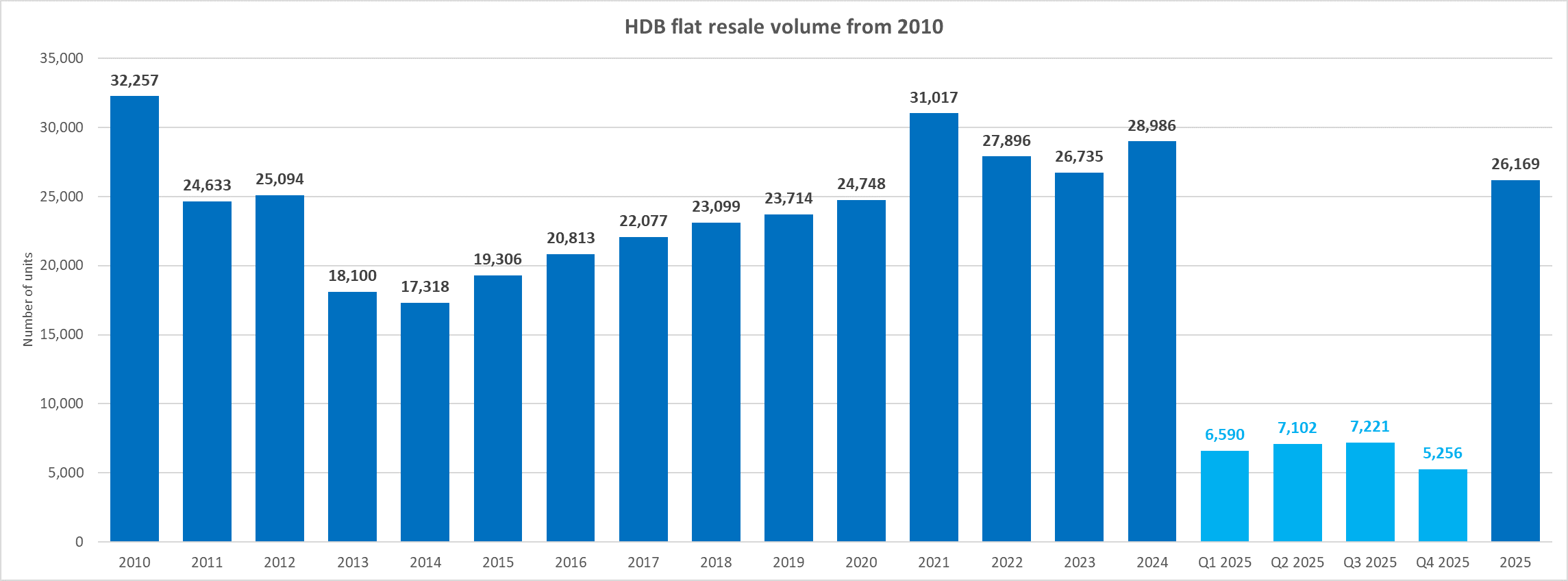

The HDB said there were 5,256 flats resold in Q4 2025, marking a 27.2% decline from the 7,221 units transacted in Q3 2025. It is also the weakest quarterly HDB resale volume since 3,426 flats were resold in Q2 2020. All in, 26,169 public housing flats were resold in 2025 - down by 9.7% from the 28,986 resale flats transacted in 2024.

Table 2: HDB Resale Price Index

Quarter | QOQ % change | YOY % change |

Q1 2022 | 2.4% | 12.2% |

Q2 2022 | 2.8% | 12.0% |

Q3 2022 | 2.6% | 11.6% |

Q4 2022 | 2.3% | 10.4% |

Q1 2023 | 1.0% | 8.8% |

Q2 2023 | 1.5% | 7.5% |

Q3 2023 | 1.3% | 6.2% |

Q4 2023 | 1.1% | 4.9% |

Q1 2024 | 1.8% | 5.8% |

Q2 2024 | 2.3% | 6.6% |

Q3 2024 | 2.7% | 8.1% |

Q4 2024 | 2.6% | 9.7% |

Q1 2025 | 1.6% | 9.4% |

Q2 2025 | 0.9% | 8.0% |

Q3 2025 | 0.4% | 5.6% |

Q4 2025 | 0.0% | 2.9% |

Ms Wong Siew Ying, Head of Research and Content, PropNex Realty said:

"The moderation in HDB resale price growth and softer transaction volume point to a market that is normalising after several years of healthy gains. The 2.9% price increase in 2025 is the slowest pace of growth in six years since resale prices inched up by 0.1% in 2019. Cumulatively, HDB resale prices have climbed by almost 55% from 2019 to 2025, based on the HDB resale price index. Meanwhile, 2025's total resale flat volume touched a five-year low at 26,169 units (see Chart 2).

In our view, the stabilisation in the broad HDB resale market is mainly due to the ramp up in new flat supply and the various cooling measures implemented in the past years, which together have helped to ease demand pressures and slowed price growth. That being said, the number of million-dollar resale flats sold has jumped to a new record yet again at 1,594 units in 2025 - up by 54% from the previous high of 1,035 units in 2024. We reckon this is not at odds with the slowing trend of overall price growth in the HDB resale segment, but rather continue to reflect segmentation within the resale flat market.

Chart 2: HDB resale flat volume

We note that around 91% (or 1,455 units) of the HDB flats resold for at least $1 million are located in mature towns (see Table 3), with the remaining 9% (or 139 units) in non-mature estates. The top three HDB towns for such sales in 2025 were Toa Payoh, Bukit Merah, and Queenstown which collectively saw 691 units of million-dollar resale flats. Meanwhile, the million-dollar resale flat transactions in non-mature towns were led by Hougang and Woodlands with 45 and 29 such deals in 2025, respectively.

It is likely that million-dollar resale flat transactions may remain elevated in 2026 - possibly crossing 1,000 units again - as well-located flats and units with sought-after attributes continue to command healthy demand. We expect such sales could concentrate in a narrow segment and may not materially affect pricing for the vast majority of resale flat buyers, who should still be able to find other affordable options in the wider HDB resale market.

Table 3: Number of million-dollar resale flats sold from 2012 by town classification by year, and proportion

| Mature | Non-mature | Total | Proportion | |

Mature % | Non-mature % | ||||

2012 | 2 | 0 | 2 | 100% | 0% |

2013 | 3 | 0 | 3 | 100% | 0% |

2014 | 2 | 0 | 2 | 100% | 0% |

2015 | 12 | 0 | 12 | 100% | 0% |

2016 | 20 | 0 | 20 | 100% | 0% |

2017 | 46 | 0 | 46 | 100% | 0% |

2018 | 70 |

Explore Your Options, Contact Us to Find Out More!

Selling your home can be a stressful and challenging process, which is why

it's essential to have a team of professionals on your side to help guide you through the journey. Our

team is dedicated to helping you achieve the best possible outcome when selling your home.

PropNex Realty Pte Ltd - Licence No: L3008022J Desmond Mok |

R012393I Register now for exclusive updates on this upcoming project.

| |||